Know What Every School on Your List Will Actually Cost.

Before Your Student Applies.

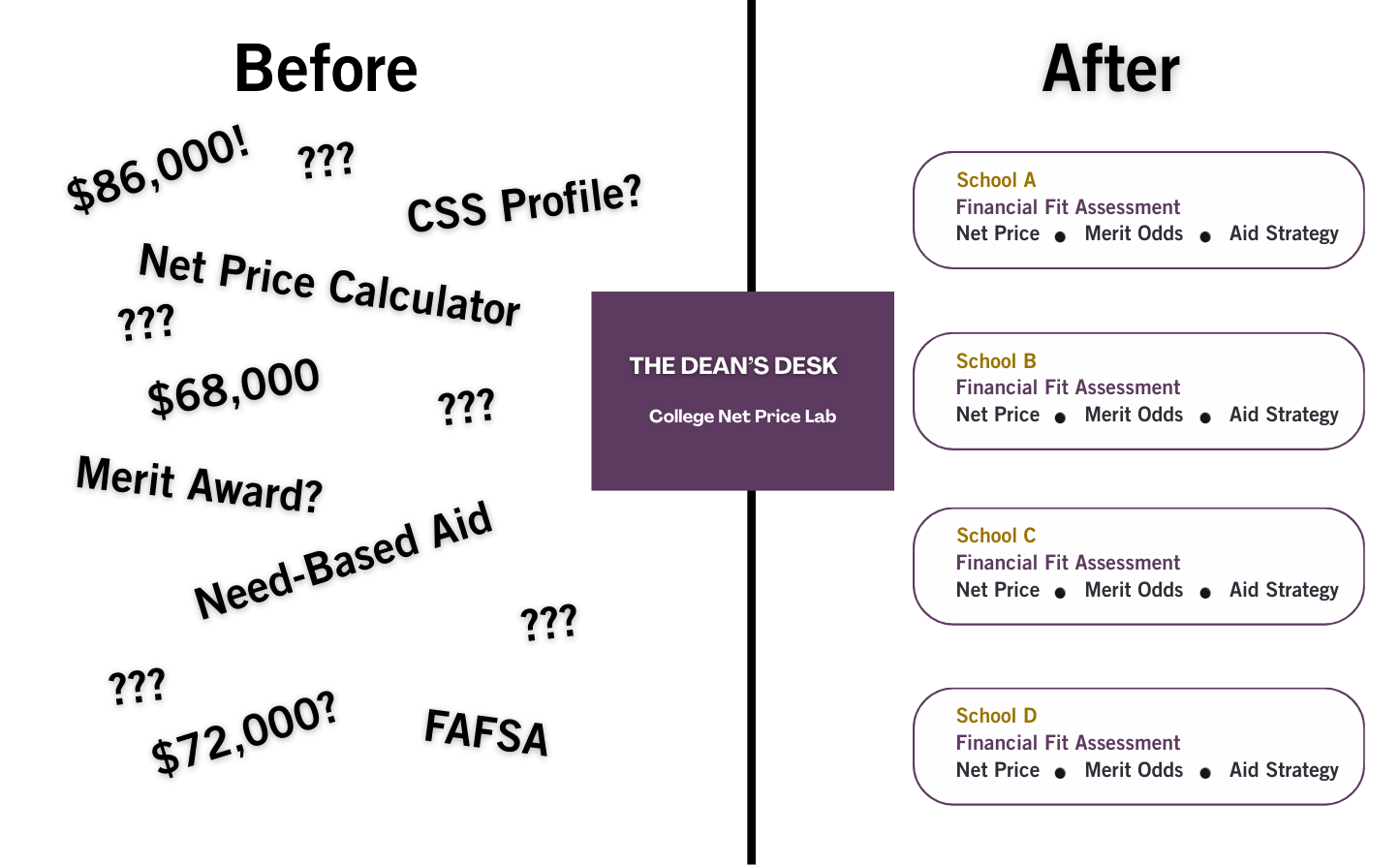

The College Net Price Lab teaches middle-income families how to assess the full financial fit of each school on their student's list, before applications are submitted — when families still hold the most leverage.

The April Surprise No One Warns You About

Every year, thousands of families go through the same painful cycle. Their student applies to schools the family hopes they can afford, gets in, falls in love — and then the financial aid offer arrives. The net price calculator said $45,000. The actual package says $68,000. Per year.

By April, the leverage is gone. The emotional attachments are made. The conversation isn't about choosing strategically — it's about taking something away. To avoid breaking their child's heart, families take on massive debt — setting up financial strain that follows them for years.

This happens because the financial aid system is genuinely complex. Each school calculates your cost differently. Net price calculators vary wildly in quality. Merit aid follows patterns most families don't know to look for. And families with any financial complexity — home equity, business ownership, divorce, rental properties — face an even wider gap between what the calculator predicts and what the actual offer says.

Families who plan strategically make financial decisions before applications are submitted— when they still have the most control.

Affordability is not the same as Financial Fit.

Affordability asks: "Can we pay?"

Financial fit asks: "Will this school make it possible?"

A financially fit school is one where there's a realistic path to an offer your family can actually accept. That path looks different at every school — and it depends on your student's positioning, your financial picture, and the school's aid strategy.

Knowing which schools fit financially before you apply is what gives you real choices in April.

You can be eligible for merit aid and only have a 6% chance of getting it. You can be ineligible for need-based aid everywhere and still build a list where your student gets $25K-$35K in merit at multiple schools. The difference is understanding eligibility vs. probability — and knowing how to read the data.

What You’ll Learn Inside The College Net Price Lab

Five Weeks. Five Modules. A Complete System for Evaluating College Financial Fit.

-

Most families are told to run the net price calculator and trust the number. That advice fails middle-income families in specific, predictable ways. This module covers why the "donut hole" makes financial planning critical, what net price calculators actually measure (and miss), and why merit aid is a strategic pricing tool — not an academic reward. You'll leave understanding the Financial Fit System and how you'll apply it over the next five weeks.

-

A school can advertise "$45 million in merit scholarships" and that number can be almost meaningless for your family. This module teaches you how colleges actually use aid as a pricing tool, how to find and read the Common Data Set for any school, how to calculate real merit aid distribution percentages, and how to assess whether your student is positioned to receive merit at a specific institution. You'll do a live CDS walkthrough and leave able to analyze any school's merit behavior yourself.

-

The same family can get completely different cost estimates at two similar schools — because each school uses a different formula. This module covers the real differences between FAFSA-only and CSS Profile schools, how home equity policies can add $15,000-$25,000 to your expected cost at certain institutions, and how to run a strategic NPC testing protocol when your family has complexity factors like business ownership, divorce, rental properties, or retirement contributions. You'll use the course workbook's home equity database (100+ schools) to check policies for every school on your list.

-

This is the session that changes everything.

I'll take a realistic family profile — similar income, similar assets, similar complexity to yours — and walk through actual schools on their list, live. For each school, we'll pull the CDS data, check the home equity policy, run the NPC testing protocol, assess the student's merit positioning, and make a call: Viable, Stretch, or Eliminate.

You'll watch schools that look affordable turn out to be impossible. You'll see schools that seem expensive become viable because of favorable policies and strong merit odds. And you'll see patterns emerge — FAFSA-only schools protecting families from asset penalties, high merit distribution rates signaling real opportunity, need-only schools with no path for middle-income families. Then you'll apply the same process to your own student's list using the course workbook.

-

The hardest part of this process isn't the data — it's the conversations. How do you talk to your student about financial boundaries without making them feel limited? How do you eliminate a school they love? What do you say in April if an offer comes in low? This module gives you specific language, scripts, and frameworks for every stage: the initial money conversation, the list-building discussion, and the April decision. You'll also learn when financial aid appeals work (and when they don't), how to frame an appeal, and how to set expectations so April feels like a confident decision, not a scramble.

After The College Net Price Lab, you’ll be able to:

✅Run and interpret a net price calculator accurately — so you know what each school is likely to actually cost your family, not the sticker price

✅Read a school's Common Data Set to understand its financial aid behavior — who they give money to, how much, and whether your student is likely to benefit

✅Identify whether a school uses federal or institutional methodology — and understand why that matters or your specific financial situation

✅Distinguish between what Jeffrey Selingo calls buyer and seller schools — so you can build a list that includes schools where your student has real leverage for merit aid

✅Evaluate merit aid strategically — understanding how schools use it as a pricing tool and how to position your student to receive it

✅Build a college list filtered for financial fit, not just academic fit — where every application is an informed, intentional decision

✅Prepare for difficult financial conversations — with your student about what's realistic, and with financial aid offices if you need to appeal

✅Navigate complex financial situations — divorce, small business ownership, rental properties, home equity, retirement assets — and understand how each affects your aid profile differently depending on the school

You Could Figure This Out Yourself.

Here's Why Most Families Don't.

Free information exists — but it's scattered, incomplete, and mostly written by people who've never worked inside an enrollment office.

The College Net Price Lab is the first systematic framework built specifically for middle-income families, and taught by a former enrollment management dean.

High school college counselors and private admissions consultants focus on essays, applications, and fit — financial aid strategy isn't what they do.

The College Net Price Lab is for you if:

✅Your household income is between $250K-$400K and you've already figured out need-based aid isn't going to move the needle

✅ Your student is a junior or rising senior and the college list is starting to take shape

✅You want to make financially informed decisions before applications are submitted — not after the decision letters arrive

✅You've run a net price calculator and wonder if you’re getting an accurate reading

✅You have complexity factors: home equity, business income, divorced parents, rental properties, or retirement contributions

The College Net Price Lab is NOT for you if:

⛔You're looking for FAFSA or CSS Profile form completion help

⛔You want someone to build your student's college list for you

⛔Your student is already a senior with applications submitted

⛔You're looking for admissions essay help or application strategy

The College Net Price Lab launches Spring 2026 (May/June) with a founding cohort limited to 50 families.

Regular Price: $3,495

Founding Cohort: $2,495

ONLY 50 SPOTS AVAILABLE. Once the course is filled, participants will go on a waitlist for the next live offering in August/September at full price.

$1,000 deposit secures your place in the Spring 2026 cohort (May/June). Remainder due 7 days before the course begins.

What's included:

• 5 live teaching sessions with Christina (60-75 minutes each, via Zoom)

• Weekly Q&A Sessions (60 minutes, via Zoom)

• The Financial Fit System framework and all course materials

• The Financial Fit Workbook — Home Equity Database (100+ schools), College Comparison Organizer, and Financial Fit Assessment Tool

• Private cohort community (closed Facebook Group) with Christina

• All session recordings

MONEY BACK GUARANTEE

Attend the first two sessions. If you don't come away with a clearer picture of your financial fit and a concrete framework for evaluating your student's list, email me directly and I'll refund every dollar.

No forms. No conditions. No "you didn't do the work" clauses.

Your Instructor

Christina Lopez spent 20 years in college admissions and enrollment management, including 9 years in leadership at Barnard College — progressing from Director of Admission to Dean of Enrollment Management. In those roles, she chaired admission committees, signed admit letters, and set institutional enrollment and financial aid strategy — balancing a financial aid budget against the college's revenue goals.

She built The Dean's Desk for middle-income families caught in the financial aid "donut hole" — earning too much for need-based aid, but facing college costs that have grown far beyond what most families can comfortably carry for four years. Most families are told to run the net price calculator and trust the number, without understanding what it actually measures and what it completely misses.

The Financial Fit System translates 20 years of insider enrollment management knowledge into a practical framework families can use — so you evaluate the true cost of college for every school on your list before applications are submitted, when you still have the most control in the process.

Frequently Asked Questions

-

The founding cohort begins Spring 2026 (May/June) and runs for five weeks. Exact dates will be shared with depositors as we get closer to launch.

-

One 60-75 minute live session per week, plus an optional 60-minute Q&A session. You'll also spend time between sessions applying the system to your student's college list. Plan for about 3-4 hours per week total.

-

Every teaching session is recorded and available within 48 hours. You'll also have the Facebook Group and Q&A Sessions to ask questions on your own schedule.

-

No. This is a live group course. I teach the framework and you apply it to your family's situation using the tools and materials provided. You can ask questions during live sessions, Q&A sessions, and in the closed Facebook group.

-

The course is designed for families with juniors who are actively building their college list. If your student is a freshman or sophomore, you're welcome to join — you'll be ahead of the curve.

-

The $1,000 deposit reserves your spot. The remaining $1,495 is due 7 days before the first session. If you need to discuss timing, email hello@thedeansdesk.com.

-

Yes. Attend the first two sessions. If the course isn't the right fit, email me for a full refund. No questions asked.

-

No. Counselors and IECs help with admissions — essays, applications, school fit. This course covers the financial side: understanding what schools will actually cost and building a financially viable list. They complement each other.

-

That's actually ideal timing. The Financial Fit System helps you build the list with financial fit as a factor from the start, rather than retrofitting it later.

-

If you can read Common Data Set for merit distribution, identify what financial aid methodology an instituion is using, understand how home equity caps affect your expected contribution, and run a strategic NPC testing protocol — you might not need this. If any of that sounds unfamiliar, this course will fill significant gaps.

Your student's list exists right now. The financial picture is already forming.

The families who get real choices in April started asking the right questions before applications were submitted.

Reserve your spot today.

Founding Cohort: $2,495 (reserve with $1,000 deposit)

Questions? Email questions@thedeansdesk.com